Tax on tip

KNOWLEDGE NUGGETS

Tax

An amount of money that a government requires people to pay according to their income, the value of their property, etc., and that is used to pay for the things done by the government.

Income Tax

Income Tax in India is governed by Entry 82 of the Union List of Seventh Schedule to the Constitution of India, empowering the Central Government to tax the income.

Income Tax Law

Income-tax law consists of the Income Tax Act, 1961, Income-Tax Rules 1962, circulars and notifications issued by the CBDT, Annual Financial Acts, and judicial pronouncements by the Supreme Court, High Courts, and Income-Tax Appellate.

Tax Deducted at Source

The concept of “Tax Deducted at Source”, commonly known as TDS ensures a regular flow of revenue to the Government. The payer of income is required to deduct tax from certain payments at the prescribed rates and deposit it to the credit of the Central Government within the prescribed time.

Suspense Account

The term “suspense account” can have several different meanings, depending on the context. In the business world generally, a suspense account is a section of a company’s financial books where it can record ambiguous entries that need further analysis to determine their proper classification.

Income Tax Return

This is the form to report to the Income Tax Department the income earned during the financial year. Various forms can be used to report the income and depend on the sources of income and the type of assessee.

Accrue

To accrue means to accumulate over time—most commonly used when referring to the interest, income, or expenses of an individual business. Interest in a savings account, for example, accrues over time, such that the total amount in that account grows. The term accrue is often related to accrual accounting, which has become the standard accounting practice for most companies

Form 16

This is a certificate issued by the employer and contains the information necessary to prepare and file your Income Tax Return. Part A of the form mentions the employer and employee’s full address, their Permanent Account Number (PAN), the Tax deduction Account Number (TAN) of the employer, the amount of tax deducted and deposited by the deductee for the relevant Assessment Year, and challan numbers. Part B mentioned details of salary paid, any other income, exemptions & deductions availed, and tax deducted.

Depreciation

Depreciation is an accounting practice used to spread the cost of a tangible or physical asset over its useful life. Depreciation represents how much of the asset’s value has been used up in any given time. Companies depreciate assets for both tax and accounting purposes and have several different methods to choose from

Advance Tax

The scheme of advance tax requires every taxpayer to estimate his current income, and if tax liability on such estimated income exceeds the specified limit, the taxpayer is required to pay the estimated tax in installments during the financial year itself

Gross Total Income

Gross Total Income includes salary income, income from house property, profit and gains of business & profession, capital gain, and income from other sources. These are computed after adjusting for the relevant exemptions under each head, such as HRA, interest paid on home loans, eligible allowances, etc.

Self Assessment Tax

‘Self-Assessment’ means the calculation of total income and tax liability thereon by the assessee himself. It is after 31st March but before the filing of the return of income.

Long-Term Capital Asset

In general, a capital asset is considered ‘long-term’ if it is held by a taxpayer for more than 36 months, immediately preceding the date of its transfer. The general rule has a few exceptions wherein an asset, held for not more than 36 months but more than 12 or 24 months, is treated as a long-term capital asset.

- However, Unlisted Shares of a company (equity shares or preferences shares) and an immovable property, being land or building or both are treated as long-term capital assets if they are held for more than 24 months immediately preceding the date of transfer.

- Further, listed shares of a company (equity shares or preference shares), Listed securities (debentures, bonds, derivatives, etc.), Units of UTI (listed or unlisted), Units of equity-oriented fund (listed or unlisted) and Zero Coupon Bonds (Listed or Unlisted) are treated as a long-term capital asset if they are held for more than 12 months immediately preceding the date of transfer.

Short-Term Capital Asset

In general, a capital asset is deemed as ‘short-term’ if it is held by a taxpayer for not more than 36 months, immediately preceding the date of its transfer. The general rule has a few exceptions wherein an asset, held for not more than 12 months or 24 months, is treated as a short-term capital asset.

- However, unlisted shares of a company (equity shares or preferences shares) and an immovable property, being land or building or both are treated as short-term capital assets if they are held for not more than 24 months immediately preceding the date of transfer.

- Further, listed shares (equity shares or preference shares), Listed securities (debentures, bonds, derivatives, etc.), Units of UTI (listed or unlisted), Units of equity-oriented fund(listed or unlisted), and Zero Coupon Bonds (Listed or Unlisted) are treated as a short-term capital asset if they are held for not more than 12 months immediately preceding the date of transfer.

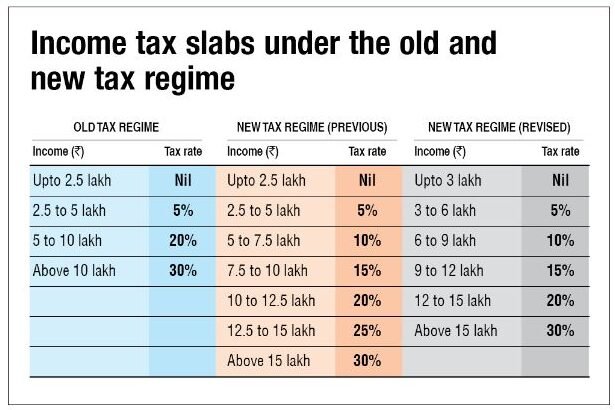

New Regime Vs. Old Regime: